With an EPO, you can just receive services from service providers within a specific network. Nevertheless, exceptions can be made for emergency situation care. Another attribute of an EPO plan is that you may be required to choose a medical care doctor (PCP). This is a basic practitioner who will supply preventative care and treat you for small diseases. In addition, with an EMO plan, you usually do not require to get a referral from your PCP in order to see a specialist doctor. A high-deductible health insurance (HDHP) has a couple of essential characteristics. As its name suggests, it has a greater yearly deductible than other insurance plans.

High-deductible health plans typically have lower monthly premiums. This kind of plan is ideal for young or usually healthy people who do not anticipate to demand healthcare services unless they experience a medical emergency or an unforeseen mishap. How much is mortgage insurance. The last defining feature of a high-deductible health plan is that it provides access to a tax-advantaged Health Cost savings Account (HSA). An HSA is an account that subscribers can contribute funds to that can later be used for medical costs that their high deductible health plan does not cover. The advantage of these accounts is that the funds are not subject to federal income taxes at the time of the deposit.

A portion of services that subscribers receive is spent for with pre-tax dollars. Like other high-deductible health care strategies, consumer-driven health insurance have higher yearly deductibles than other medical insurance plans but the subscriber pays lower premiums every month. A point of service (POS) plan provides various benefits to subscribers based upon whether they use favored suppliers (in-network service providers) or suppliers beyond the favored network (out-of-network companies). A POS plan consists of functions of both HMO strategies and PPO plans. A short-term insurance coverage policy covers any gap you might experience in coverage if, for example, you change tasks and your new business strategy does not kick in immediately.

Get This Report about How Much Is Long Term Care Insurance

Term lengths vary by state, and in some U.S. states, you might be qualified for a short-term strategy for up to 12 months. Short-term health insurance coverage is likewise called short-lived medical insurance or term health insurance. It can be beneficial if you're changing tasks, waiting to become qualified for Medicare protection, or waiting out the designated open registration period for a plan. Under a short-term insurance coverage plan, your spouse and other eligible dependents might also be covered. Nevertheless, one crucial caveat of a short-term insurance coverage plan is that sometimes, pre-existing conditions can disqualify you from protection. The meaning of a pre-existing condition differs depending upon the state you live in, however it is generally defined as something you have actually been diagnosed with or received treatment for within the last two to five years.

In order to certify, you must receive a challenge exemption from the government. Catastrophic health insurance coverage generally has lower premiums than other health insurance plans. These types of plans are intended for people who can not afford to spend quite money monthly on insurance premiums but who don't wish to lack insurance in the event of a major mishap or health problem. While catastrophic health insurance plans may have low monthly premiums, they typically have the greatest possible deductibles. Once you've selected the kind of strategy that is best for you, you'll require to determine just how much you can manage to pay as a deductible.

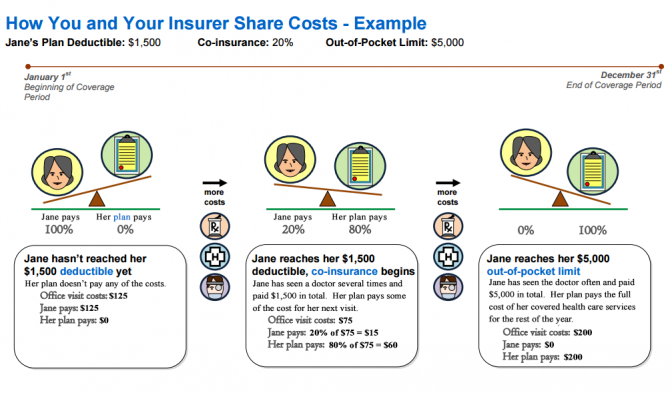

What can you pay for to pay in out-of-pocket medical expenditures each year? With many medical insurance strategies, the higher your deductible is, the lower your regular monthly premium will be. If your regular monthly capital is low, you might have to go with a higher deductible. Another crucial Find more info factor to consider when choosing an insurance coverage strategy is the plan's out-of-pocket maximum. After you've invested this amount on deductibles and medical services through co-payments and co-insurance, your health insurance will pay the entire cost of covered advantages. While many individuals are scared by the possibility of purchasing their own insurance coverage timeshare jobs versus enrolling in an employer-sponsored strategy, some research studies have shown that it can end up being more budget-friendly than employer-sponsored plans.

Things about How Does Whole Life Insurance Work

It was $1,725 for household protection. Conversely, according to the Kaiser Household Structure, if you were to purchase your own insurance beyond an employer-sponsored plan, the average expense of individual medical insurance was $440. For families, the typical monthly premium was $1,168. In addition, if you end up purchasing coverage through the Medical insurance Market, you might receive a Cost-Sharing Decrease subsidy and Advanced Premium Tax Credits. These can reduce the quantity you pay for premiums, as well as decreasing your deductible, and any co-payments and co-insurance you are accountable for. You have a number of alternatives when it comes to purchasing private medical insurance.

It is recommended that you see what the basic Medicare plan covers and after that take a look at options for ways to supplement Medicare through Medigap and Medicare Advantage policies. When considering Medigap or Medicare Advantage coverage, it's crucial to understand how both work kinds of coverage operate in conjunction with standard Medicare coverage (How does cobra insurance work). As a result of the Affordable Care Act (ACA), the Health Insurance Market was developed in 2014. You can check out the Medical insurance Market website to discover more about the options for health insurance protection that are offered where you live. You can likewise figure out if you certify for any subsidy and request it.

Typically, it is in between November 1 and December 15 every year, although numerous occasions might result in the open enrollment duration being extended or resumed. On Jan. 28, 2021, President Joe Biden signed an executive order to execute an Unique Registration Duration, reopening the federal insurance market (healthcare. gov) from Feb. 15 through May 15, 2021. The website includes information about personal plans that are available for purchase beyond the Market. Nevertheless, if you purchase a plan outside the ACA's Market, whether during open registration or not, you will not be qualified for any aids available under the ACA.

Some Known Questions About How To Cancel Health Insurance.

This is called an Unique Enrollment Duration. You may be qualified for a Special Enrollment Period if you experience a household modification, including marrying or divorced, having or embracing a kid, a death in your family, moving, losing your medical insurance, remaining in a nationwide catastrophe, or experiencing a special needs. The American Rescue Strategy of 2021 increased subsidies for ACA strategies for lower-income Americans and broadened subsidies to consist of some subsidies at greater earnings levels. You can check out the websites of significant medical insurance companies in your geographic Great post to read area and search offered alternatives based upon the type of coverage you prefer and the deductible you can pay for to pay.